UPDATE 18 December 2021: Provident has confirmed that it’s fully closing its doorstep lending enterprise (Provident Private Credit score) on thirty first December 2021. When you have any debt with Provident at this level will probably be written off fully and you’ll not be required to repay it. When you have a steady cost authority in place to repay your debt then Provident will cancel it robotically beforehand. Should you make funds after this date then they are going to be repaid to you.

Provident Monetary Plc is the biggest subprime lender within the UK based in Bradford in 1880. During the last 140 years, the corporate has grown and tailor-made its core lending enterprise to raised serve the wants of its clients who had been underserved by mainstream banks and credit score firms. Of its three divisions, its Client Credit score Division (CCD) that operates its house credit score (Provident loans) and on-line (Satsuma Loans) is probably its most vital. So, it’s all the extra stunning that Provident has been fighting house collected loans in the previous few years.

Provident’s Doorstep Lending Enterprise

Provident’s doorstep loans enterprise gives small worth loans to people who find themselves typically excluded from mainstream credit score options, whose incomes are sometimes beneath the UK’s common and extra probably than to not lease their house. Maybe most significantly the purchasers do not need the luxurious of financial savings to buffer them. Therefore the entry to small loans that they will repay on a weekly foundation has been vital. The common mortgage dimension is round ¡ê300. At any cut-off date Provident is lending to round 300,000 clients.

As of December 2020, the UK house credit score market was value ¡ê592m and Provident managed 39% of that. Over the identical interval, the high-cost short-term market was valued at ¡ê184m and Satsuma HCSTC managed 8% of this market. A portion of the UK market is met by native and regional suppliers. Provident is considered one of three nationwide suppliers, the others being Morses Membership and Loans at House.

Provident Is Closing Its Client Credit score Division

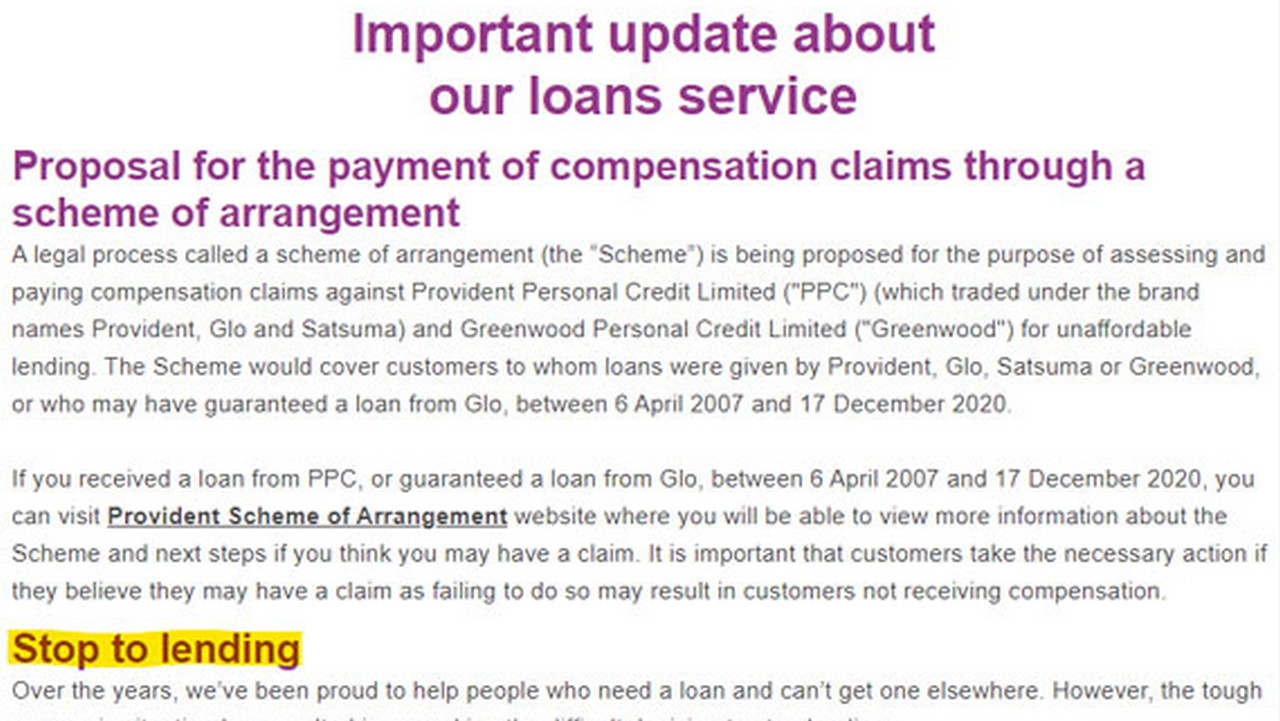

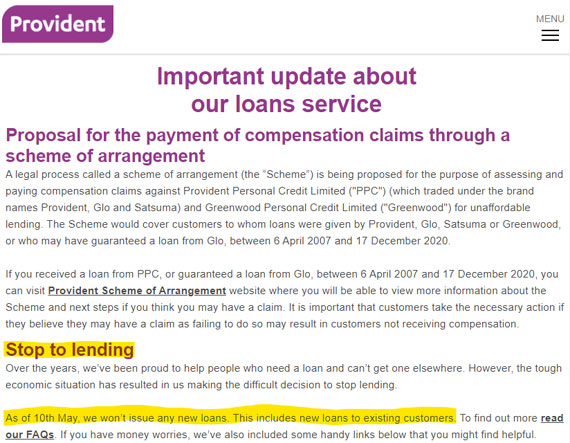

On 10 Might 2021, the Provident introduced it was stopping lending to each new and present clients because it contemplated inserting the division right into a managed run-off or disposal. The one exception could be for purchasers who had already utilized for loans and had signed the mortgage agreements. However why such a radical announcement? What’s gone unsuitable?

Among the division’s weak spot stems from errors it made in 2017. Again then it selected to maneuver from a self-employed workforce of brokers to a brand new employed workforce supported by new know-how. Most of the brokers selected to go away the trade moderately than change into employed. Others had been picked off by their rivals. And the brand new assist software program created chaos for the collections course of. The 2 issues mixed such that the worth of the enterprise was considerably decreased. And the issues endured over time.

On the again of this enterprise weak spot, Provident’s competitor Non-Customary Finance (NSF), homeowners of “Loans at House”, tried an unwelcome takeover of them in 2019. If nothing else this was a distraction that Provident may have completed with out. Provident managed to discourage NSF however extra harm was completed.

Rather more just lately?Provident has highlighted two different elements which have triggered its resolution to exit the doorstep lending enterprise:

Buyer Complaints

Provident clients have more and more been launching mis-selling complaints by way of Claims Administration Corporations. In line with the claims, clients faulted the best way Provident performed its affordability and sustainability checks when handing out loans. The Monetary Conduct Authority (FCA) jumped in to research the complaints particularly for loans issued between February 2020 to February 2021. Within the first half of 2020, compensations for buyer complaints price PFG ¡ê25million an enormous leap from ¡ê2.5million in the identical interval the earlier yr.

Monetary Struggles

Even earlier than Covid-19, the Client Credit score Division had begun exhibiting indicators of economic battle. When the pandemic hit, the operations worsened leading to a ¡ê74.9m adjusted loss earlier than tax loss for the division in 2020 in comparison with a ¡ê20.8m loss recorded in 2019.

What Taking place Now?

To assist tackle the affect of the rising shopper claims on its Client Credit score Division, PFG on 15 March 2021 launched a Scheme of Association, a authorized technique to assist an organization to restructure and assist it from monetary misery.

Below the Scheme of Association, Provident has sought to deal with claims arising from historic lending. These are claims regarding loans that had been made between 6 April 2007 and 17 December 2020. Provident put aside ¡ê50m for the Scheme claims and an extra ¡ê15m to offset the Scheme associated prices, bringing the entire dedication to ¡ê65m.

For the Scheme to be operational, it wanted to be permitted by the purchasers with redress claims and sanctioned by the Excessive Courtroom. The affected collectors are roughly 4.2 million.

The lender had warned that failure to have the Scheme permitted, the Client Credit score Division must be liquidated or put beneath administration. This might additionally imply that the purchasers with redress claims could find yourself not receiving any cost.

In line with the Provident Monetary Group board, the Scheme of Association is the perfect wager and would make sure the pursuits of all events – Client Credit score Division, the Provident Monetary Group, and stakeholders – are secured. Key dates have included:

- 22 April 2021 was the primary court docket listening to the place the Courtroom dominated that CCD organise a gathering with the collectors of the Scheme to deliberate on the deserves of the Scheme.

- 17 Might 2021, the voting portal was opened to permit previous and current CCD clients and the Monetary Ombudsman Service to vote on the Scheme.

- 19 July 2021, the Scheme Assembly as supplied for by the Courtroom was held nearly and attended by over 428,000 collectors. ?Of those, 420,000 (98.1%) voted in favour of the Scheme.

- 30 July 2021, the Excessive Courtroom in its sanction listening to permitted the Scheme of Association by Order of 4 August 2021. Which means that PFG will go forward with the implementation of the Scheme and opening of the portal.

The FCA had its reservations about the usage of a Scheme of Association. They didn’t need shoppers to undergo loss (i.e. get considerably much less compensation than they’re owed as per their redress claims), however when this was in comparison with the entire insolvency of Provident Private Credit score Restricted, the regulator determined to not transfer to court docket to dam the Scheme of Association.

What’s Subsequent?

The Scheme turned binding on 5 August 2021. Following the opening of the portal, clients may have till the tip of February 2022 to submit their claims. In the event that they fail to take action they are going to lose their proper to compensation.

Provident expects that every one compensation claims may have been assessed, settlements made, and the Scheme closed by the latter a part of 2022.